You can find a German version of the report here.

Germany’s planned LNG import terminals are not necessarily required to compensate for the loss for pipeline imports from Russia, when considering what is necessary to meet the country’s climate targets.

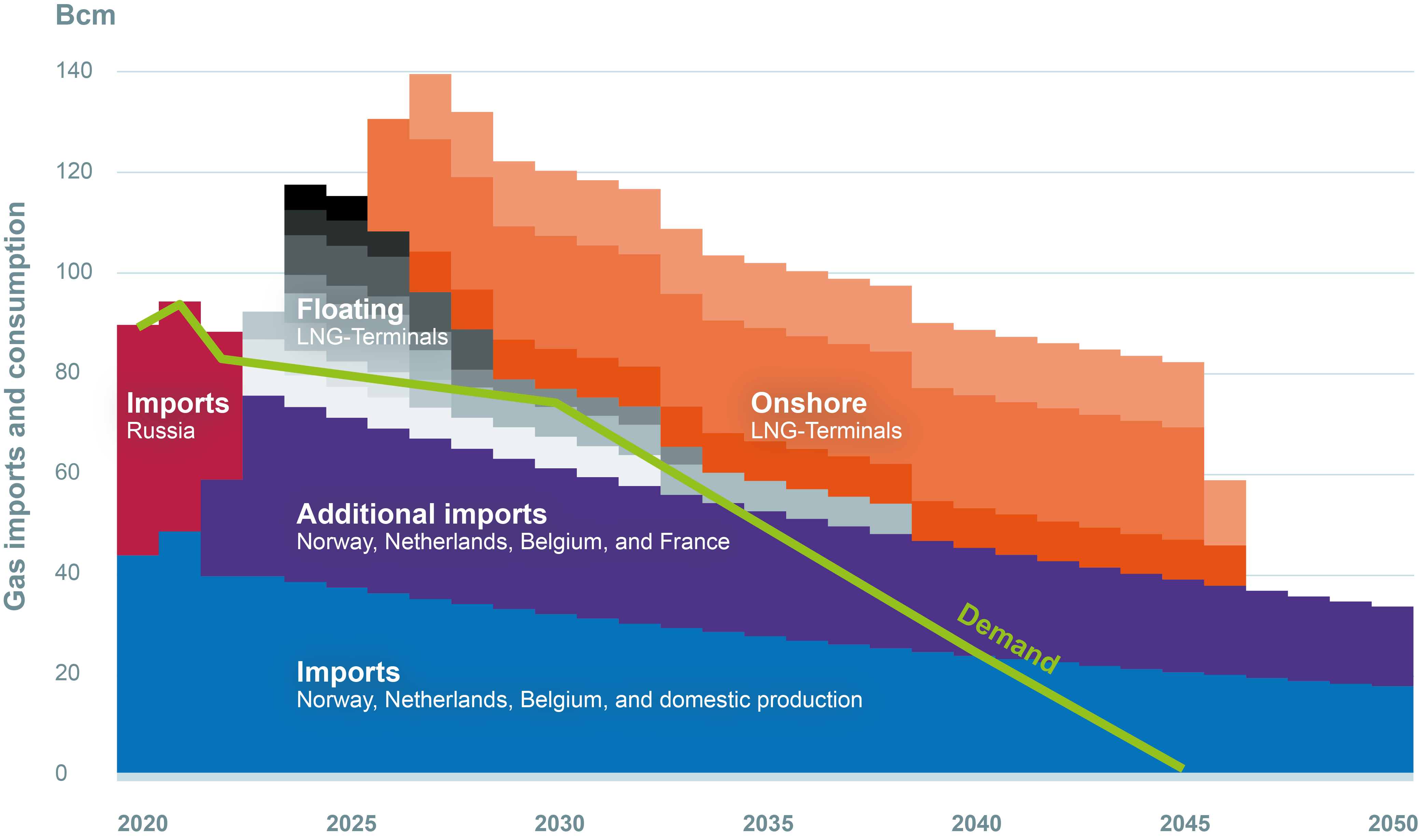

The construction and operation of all currently planned LNG terminals would not only be in conflict with Germany’s national climate targets, it would also constitute a breach of national legislation and international commitments under the Paris Agreement. Gas consumption in Germany in 2022 is estimated to be 83 bcm, around 12% lower than in 2021. The decrease in gas consumption is primarily the result of energy efficiency measures and mild temperatures. German gas consumption must steadily fall for the country to reach its goal of climate neutrality by 2045 - by around a fifth from current levels by 2030, by half by 2035, and to almost zero by 2045.

With continued efforts to save, no new LNG terminals would be needed.

If imports from neighbouring countries remain at the same level as in recent months, Germany could draw on pipeline imports of around 86 bcm per year. In combination with continued energy efficiency measures to reduce demand for gas, no new LNG terminals would be needed. Germany could seek agreements with its neighbours to maintain high exports in the short term. At the same time, Germany could strengthen energy efficiency measures to meet its self-imposed reduction target, or better yet, a more stringent 1.5°C compatible reduction target.

Germany’s current strategy points in a different direction.

Eleven LNG terminals with a total capacity of about 73 bcm per year, could enable the import of 50% more gas than was sourced from Russia before the war (46 bcm per year).

Additional LNG import capacity would minimize the risk of gas shortages but would mostly not be required to match shrinking demand.

Even if net pipeline imports are assumed to decline (75 bcm in 2023, declining subsequently by 3% per year), demand exceeds imports by no more than 15 bcm per year until 2035, with a declining trend from 2030 onward. This gap could be covered either by more ambitious reductions or by three floating terminals (FSRUs). After 2035, they also would no longer be needed.

Stranded assets are likely if all LNG terminals are built.

Since a large part of the LNG terminals is supported by federal funding, taxpayers carry a share of resulting costs. With all planned terminals fully operational, Germany would be able to import nearly two-thirds more fossil gas via land and sea than it currently consumes. Pipeline gas is likely to be preferred to LNG imports because of its significantly lower cost. Terminal operators appear to be deliberately accepting stranded asset risks, presumably with the goal of securing their market share by bidding for larger contracts. The plans are oversized, even if there are intentions to eventually repurpose the terminals to import green hydrogen or ammonia.

The new LNG terminals would undermine the energy transition.

Their construction would tie up resources and attention that would then not be available for energy efficiency measures and the expansion of renewable energy.

To remain credible and set a positive international example, Germany would have to make good on its commitments and strengthen them instead of massively jeopardizing their implementation.

Germany has enshrined its climate targets internationally in the Paris Agreement and in national climate legislation. Maintaining credibility is particularly important vis-à-vis countries with which climate partnerships are being negotiated.