Rules for the implementation of Article 6 of the Paris Agreement are still under negotiation at the international level, with a key focus on reaching consensus at COP26 in Glasgow. This report aims to inform this policy making process. It explores three key unresolved issues that are closely interrelated and that have potential to impact the global net emission reductions achieved through Article 6 as well as the amount of revenues generated to help meet the adaptation needs of particularly vulnerable developing countries.

Summary:

The report explores the potential quantitative implications of different policy choices on OMGE, SOP and the transition of CDM activities and units, both in isolation and in combination with each other, with the aim to support decision-making in the context of the ongoing international climate change negotiations. We develop a simplified economic representation of the possible future Article 6 market to illustrate potential outcomes, informed by an evaluation of the possible future supply, demand and prices for ITMOs. The main focus of our analysis is on what we label “A6+ ERs”. These are credits that are subject to the application of OMGE and SOP and eligible for international transfer and use under either Articles 6.4 or 6.2 of the Paris Agreement. These units may also be used for purposes other than achieving nationally determined contributions (NDCs), such as for the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) or in the voluntary carbon market.

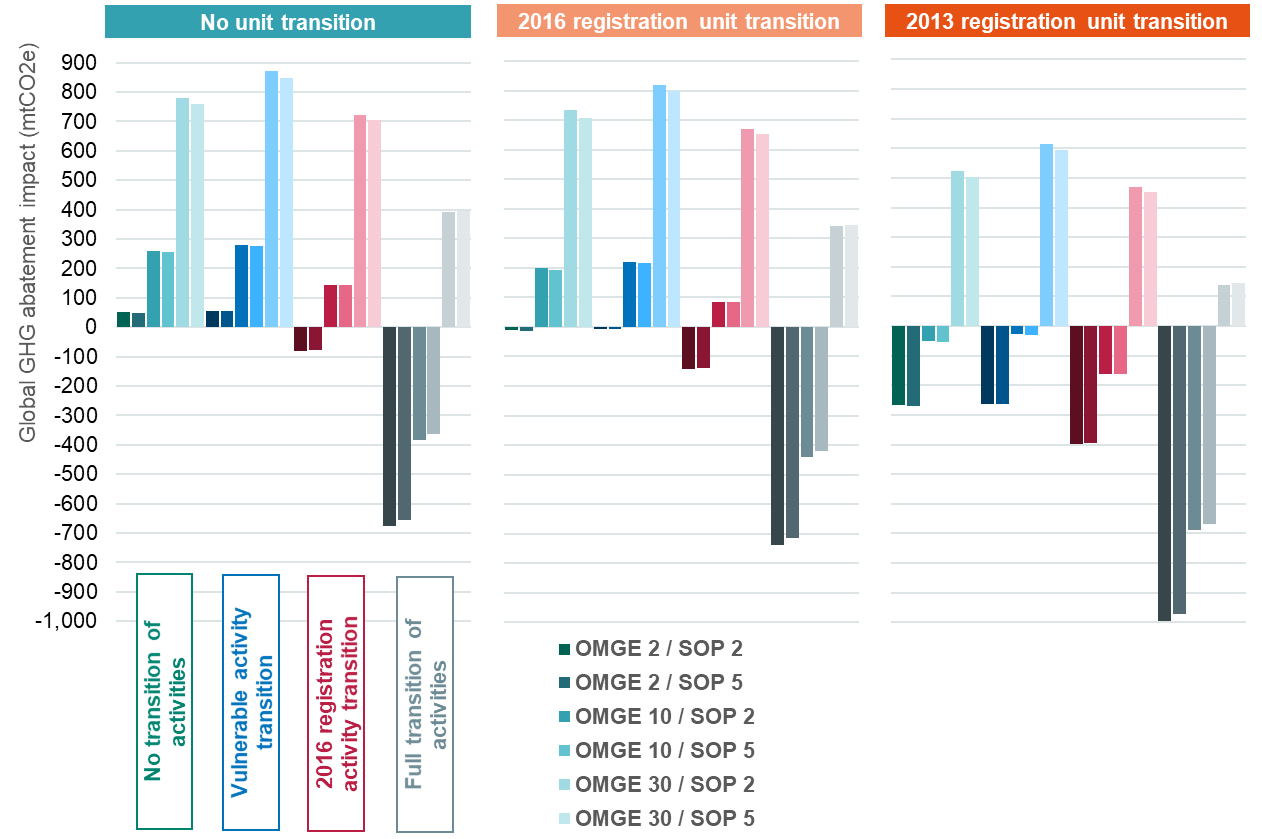

Figure: Overview of potential global GHG abatement impacts across all scenarios considered (see full report for notes)[/caption]

Figure: Overview of potential global GHG abatement impacts across all scenarios considered (see full report for notes)[/caption]

Key Findings:

For OMGE:

- Net global abatement increases with increasing OMGE cancellation rates across all OMGE scenarios considered, with emissions decreasing in both buyer countries as well as – to a lesser extent – host countries. A 30% OMGE rate could deliver about 800 MtCO2 of additional abatement over the period 2021-2030, avoiding roughly $45-181 billion in global damages. 800 MtCO2 is roughly equivalent to 6 months’ worth of total GHG emissions from all 46 LDC countries combined, or two years’ worth of emissions from all AOSIS countries.

- Credit prices, market revenues, and project owner profits increase with increasing OMGE cancellation rates, while buyers cost savings from using credits decrease.

For SOP:

- Higher percentage levels of SOP lead to increased levels of revenue for the Adaptation Fund across all SOP scenarios considered.

- Net global abatement is unaffected by SOP. Host country emissions increase, while buyer country emissions decrease by an equivalent amount.

- Credit prices and market revenues increase with increasing SOP rates, while project owner profits and buyer cost savings decrease.

For OMGE and SOP applied in combination, with no CDM transition:

- Global GHG abatement increases across all OMGE and SOP scenario considered, with the most pronounced impact where a 30% OMGE rate is applied.

- SOP revenues increase with higher levels of OMGE because the increase in the credit price at which the Adaptation Fund can monetise credits outweighs the reduction in the quantity of credits transacted. An SOP rate of 5% could raise €2.7- 4.6 billion in resources for adaptation over the 2021-2030 period, depending on the rate of OMGE applied (2-30%).

For CDM CP2 CER transition:

- The transition of CP2 CERs leads to an increase in global GHG emissions corresponding directly to the number of CP2 CERs transitioned (up to 320 MtCO2e if projects registered on or after 1 January 2013 were eligible for transition).

For CDM activity transition:

- CDM activity transition can either undermine the host country’s ability to achieve its NDC or increase global emissions, due to the large number of CDM project activities that are not dependent on carbon market revenues to continue abatement (by about 763 MtCO2e if 30% of all CDM projects were to transition).

- No transition or limiting transition to vulnerable CDM project activities – those at risk of discontinuing GHG abatement without carbon credit revenues – does not pose such a risk.

For combinations of CDM activity transition, OMGE and SOP:

- Scenarios in which only vulnerable CDM activities are eligible to transition lead to the largest potential reductions in global GHG emissions, but this relies on a robust assessment process for approving transition that categorically avoids authorising any activities that would continue abatement regardless.

- SOP revenues remain similar to OMGE and SOP policy combination scenarios with no activity transition.

For any differentiation between OMGE and SOP requirements for 6.2 and 6.4:

- Applying SOP and OMGE to credits issued by the Article 6.4 Supervisory Body, without applying the same elements to all ITMO transfers under Article 6.2, may jeopardise the climate mitigation and adaptation benefits sought by Article 6.4’s SOP and OMGE requirements.

This report was developed in collaboration with partners at Climate Analytics and Öko-Institut. The study was prepared at the request of the Group of Least Developed Countries and with support from a grant from the United Kingdom Department of Business, Energy and Industrial Strategy (BEIS).