Editor’s note: This is the second post in our five-part series, ‘Market Instruments Explained’, where we examine the prospects and risks of market instruments in corporate emissions accounting. In the series, we cover key debates around chain-of-custody models, commodity certificates, multi-statement GHG inventories and transition targets. By bringing together perspectives from standard-setters, companies and civil society, we aim to bring more clarity to this complex but increasingly central topic. See our first blog, where we introduce the current relevance of market instruments and the emerging concerns surrounding their use.

Key takeaways

-

Mass balance is not one method, but many. This accounting approach allows companies to track emissions reductions even when lower- and high-emission materials are physically mixed. However, the term encompasses vastly different methods with different levels of integrity.

-

Integrity depends on design choices. Seven key decisions determine whether mass balance drives genuine transformation or enables misleading claims. In particular, ‘stacked attribution’ could enable products to falsely appear lower-carbon than they actually are.

-

Standards need to set clearer safeguards. Existing standards remain vague on critical design choices. Without clear guardrails, mass balance risks delaying real decarbonisation rather than supporting the transition.

Decarbonising supply chains does not happen overnight. New low-emissions technologies or practices are often gradually applied to parts of production processes alongside existing production lines. As a result, lower- and higher-emissions materials may end up mixed together and the final product might not be purely 'low-carbon'. This creates a growing challenge for both suppliers and buyers: how should emissions reductions from mixed products be credibly tracked, monetised and counted towards progress?

In many sectors, accelerating demand for lower-emissions products has intensified this challenge. For example, a steel company may invest in a new electric arc furnace that produces steel with lower emissions than a traditional blast furnace. However, it may still feed into the same production line as legacy assets. The lower-emissions steel is physically mixed with conventional steel, rolled into the same sheets and shipped as the same product. Meanwhile, many large automakers are seeking to procure and claim near-zero steel today and are willing to purchase from these transitioning production processes, even if the final products are not technically 'low-carbon' yet.

In response to this challenge, many sectors are looking to mass balance methods for emissions accounting. In this blog post, we explore what mass balance is and show that it is not a single approach, but rather an umbrella term encompassing vastly different methods. We discuss that whether a ‘low-carbon’ product represents genuine industrial transformation or clever accounting depends heavily on which features of the mass balance approach are applied. As standard-setting bodies and regulators develop rules for these systems, it is crucial to consider these nuances.

What is mass balance and why is it being used?

Mass balance is a chain-of-custody model that tracks environmental attributes, such as emissions reductions, through supply chains even when physical products are blended. Instead of physically separating sustainable materials from conventional ones – a practice known as segregation – mass balance allows them to be mixed during production. It maintains accounting records to ensure that the qualities of materials entering the production process match those attributed to the final products.

Mass balance is not a new concept. It has a longer history in deforestation-free commodity supply chains, where its use has been highly contested. Critics argue that it may not deliver lower deforestation rates at a system-wide level and can be misleading to consumers. Under the EU Deforestation Regulation update released in April 2026, only certain types of mass balance are permitted to prove non-deforestation claims.

However, proponents of mass balance argue that its use for emissions accounting follows a different theory of change. In the case of deforestation-free sourcing, segregation is often viewed as necessary to exclude deforestation-linked commodities from the market completely. But for emissions accounting, the picture is more nuanced.

Supporters of mass balance typically make two main arguments. The first is a complexity argument: in opaque, global supply chains like agriculture, requiring segregation could be technically complicated and costly, potentially diverting resources away from mitigation efforts.

The second is an economic argument: to justify the ‘green premium’ needed to fund a technology upgrade, a supplier may need to sell a product with a significant emissions reduction. If the company can only claim the average emissions reductions across all products, the final emissions profile might be only marginally lower than conventional alternatives. This could make it challenging to charge a premium on the product as buyers might not be willing to pay the premium necessary for products with only limited emissions improvements. From this perspective, mass balance can be viewed as a bridge to fully segregated physical supply of lower-emission commodities or fuels.

Whether there is merit to these arguments depends highly on how mass balance accounting is applied in practice.

Mass balance is not a single approach

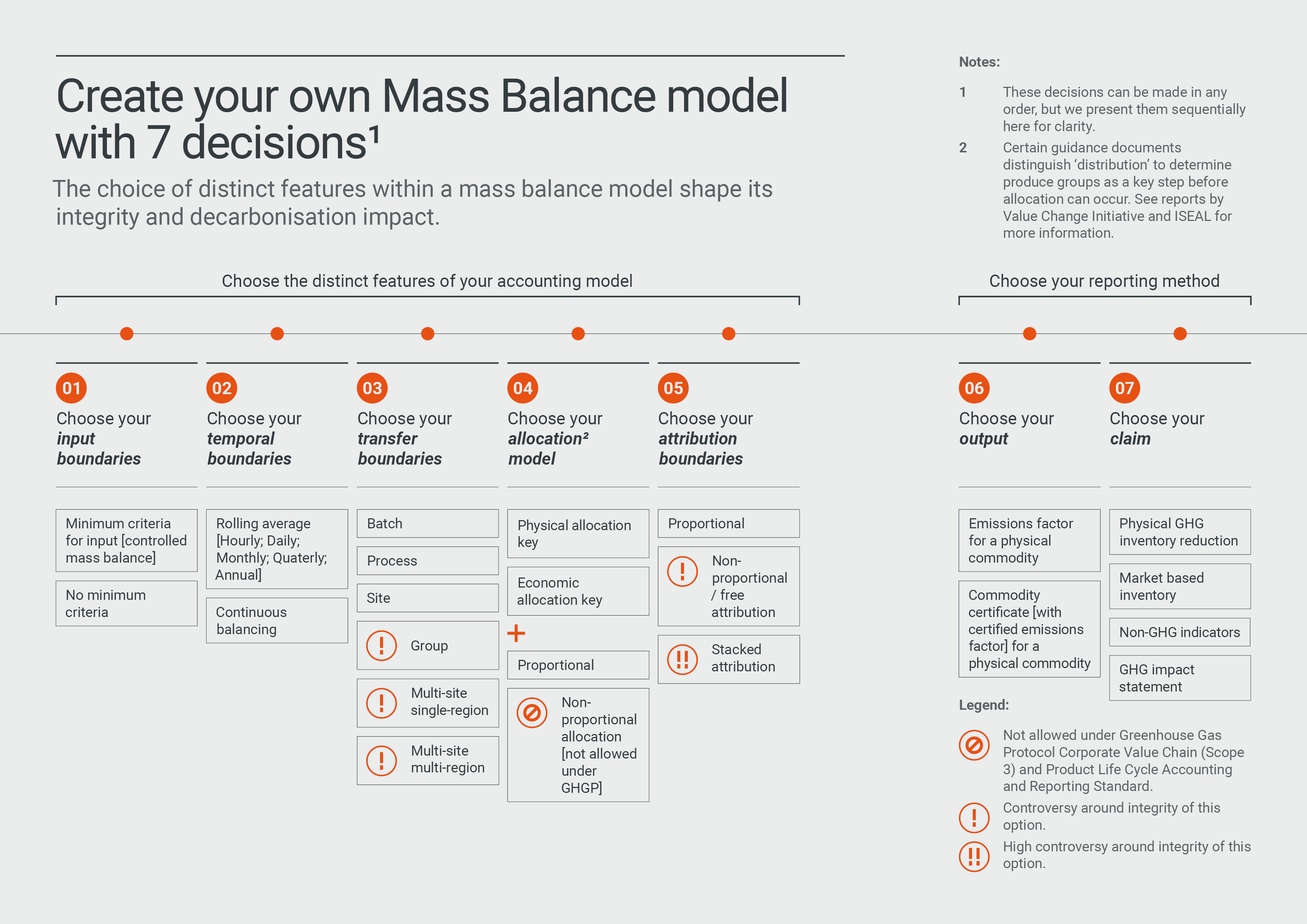

Although often presented as a singular method, mass balance actually encompasses many accounting approaches, largely based on seven key decisions (see Figure 1). These decisions are not necessarily made sequentially or independently in practice, but they are presented step-by-step here for clarity. The various options across these seven decision points create numerous possible combinations that companies could choose between, each with different implications for credibility and rigour. In the following sections, we zoom into a few key decisions in greater detail, specifically transfer boundaries and attribution, as these play a significant role in determining robustness.

Fig 1: Mass balance model with 7 decisions

Fig 1: Mass balance model with 7 decisions

Input boundaries: What products can enter the accounting pool?

The first decision concerns the criteria products should meet to enter the mass balance system. For example, what emissions profiles should the steel included in the system have? Products entering the system may either have no criteria or be required to meet a minimum set of criteria such as a benchmark on product emissions intensity. The latter approach is often referred to as ‘controlled mass balance’.

Temporal boundaries: What timeframe is considered?

The next decision concerns the time frame considered for inputs included in the mass balance system (see other analyses for more information on this topic).

Transfer boundaries: Where do we draw the line?

The third decision concerns the geographic and operational scope within which emissions profiles can be claimed, known as the transfer boundary. This choice directly affects physical connectivity – the likelihood that an end product contains any of the low-carbon material – and traceability – the ability to track product attributes through the supply chain. The question of what level of physical connectivity and traceability are necessary to ensure robust mass balance has sparked intense debate.

High-connectivity approaches, such as batch, process or single-site mass balance, maintain stronger linkages between inputs and outputs, making the presence of physical attributes more likely and verification more feasible. While they require closer monitoring, these methods enjoy broad support as they limit how far claims can extend from actual interventions.

Low-connectivity approaches, such as multi-site mass balance, allow companies to pool emissions reductions across multiple facilities and attribute them to products from any participating site. Proponents argue that this flexibility is essential to reward companies for transformation even when existing production processes span multiple locations.

However, experts, companies leading the transition and environmental advocates warn that low-connectivity approaches risk overstating the presence of ‘green’ attributes in a product, potentially leading to distorted markets and delayed transformation. More fundamentally, companies could avoid decarbonising all sites by focusing improvements only at their most cost-effective facilities and marketing these improvements widely. Allowing approaches with low physical connectivity could also discourage companies from improving commodity traceability over time. Strong traceability matters not only for enabling regulation on supply chains in the future but also for addressing other critical issues such as human rights due diligence.

Allocation model: How are emissions assigned across product groups?

The fourth decision concerns how emissions are assigned across different product groups derived from the same material, known as allocation. Certain guidance documents distinguish ‘distribution’ to determine product groups as a key step before allocation occurs. While product groups can be divided using different allocation keys, the assignment of emissions across product groups must be proportional according to the Greenhouse Gas Protocol Corporate Value Chain (Scope 3) and Product Life Cycle Accounting and Reporting Standard.

Attribution boundaries: How are emissions assigned within product groups?

The fifth decision concerns how emissions values are assigned within a specific product group when materials with different characteristics are mixed, known as attribution. Attribution has become one of the most contested aspects of mass balance accounting and there are a number of different approaches.

Proportional attribution assigns attributes evenly, while non-proportional attribution, also known as free attribution, allows selective attribution to certain outputs.

Consider the example of a fictitious steel company undergoing transition. The company invests in a new direct reduced iron (DRI) plant at a specific site. However, when lower-emissions steel is mixed with higher-emissions steel from legacy production facilities, the overall emissions remain relatively high when averaged across all products. Non-proportional attribution enables the company to assign the lower emissions factor from the steel produced in the DRI plant to a specific portion of the output, creating a ‘low-carbon’ steel product that can be sold at a premium alongside conventional steel.

Many actors describe non-proportional attribution as the ‘credit mass balance’ model. However, approaches within this category differ significantly in legitimacy. While non-proportional attribution may be reasonable when emissions reductions result from a change in technology or approach, it can also be used to misrepresent products’ emissions profiles even when no new technology has been adopted.

One particularly concerning approach is what we term ‘stacked attribution’. Stacked attribution occurs when all emission reductions from multiple inputs are attributed to a single output, resulting in a commodity that has a lower emissions factor than any individual unit of that commodity that enters the mass balance system. For example, with its Kobenable® Steel, Kobe Steel claims that it ‘reduces 100% of CO2 emissions in steel production based on the mass balance method.’ However, it is currently impossible for any steel product to be genuinely zero emissions using available technology. The claim is especially misleading in Kobe Steel's case, as their product is still produced using traditional coal-based methods with only partial substitution by DRI.

Such a claim could fundamentally mislead customers about a commodity’s real emissions footprint and delay necessary investment in and regulation of key decarbonisation technologies. As a result, some experts are warning against non-proportional attribution altogether. Critically, the current ISO standards do not yet clearly distinguish between these approaches, as discussed in the following section.

Reporting methods: Decisions on output and claim

Mass balance calculations are mainly used for two types of outputs. The first is an updated emissions factor. The second is a certificate, a tradable instrument that can either be sold together with physical products or unbundled and traded separately. This choice fundamentally shapes how emissions attributes are transferred through the value chain.

How and where emissions factors or certificates generated through mass balance can be claimed are ongoing debates within standard-setting processes. Currently, the Greenhouse Gas Protocol (GHG Protocol) only requires companies to have a physical emissions inventory (scope 1-3). However, discussions are ongoing on whether additional inventories will be allowed or required. Standards bodies and regulators are actively debating whether and which mass balance approaches are robust enough for which inventory. This decision is important as it could affect corporate climate disclosures, target-setting and compliance with emerging regulations (see the future edition of this series for more on the nuances of corporate emissions inventories).

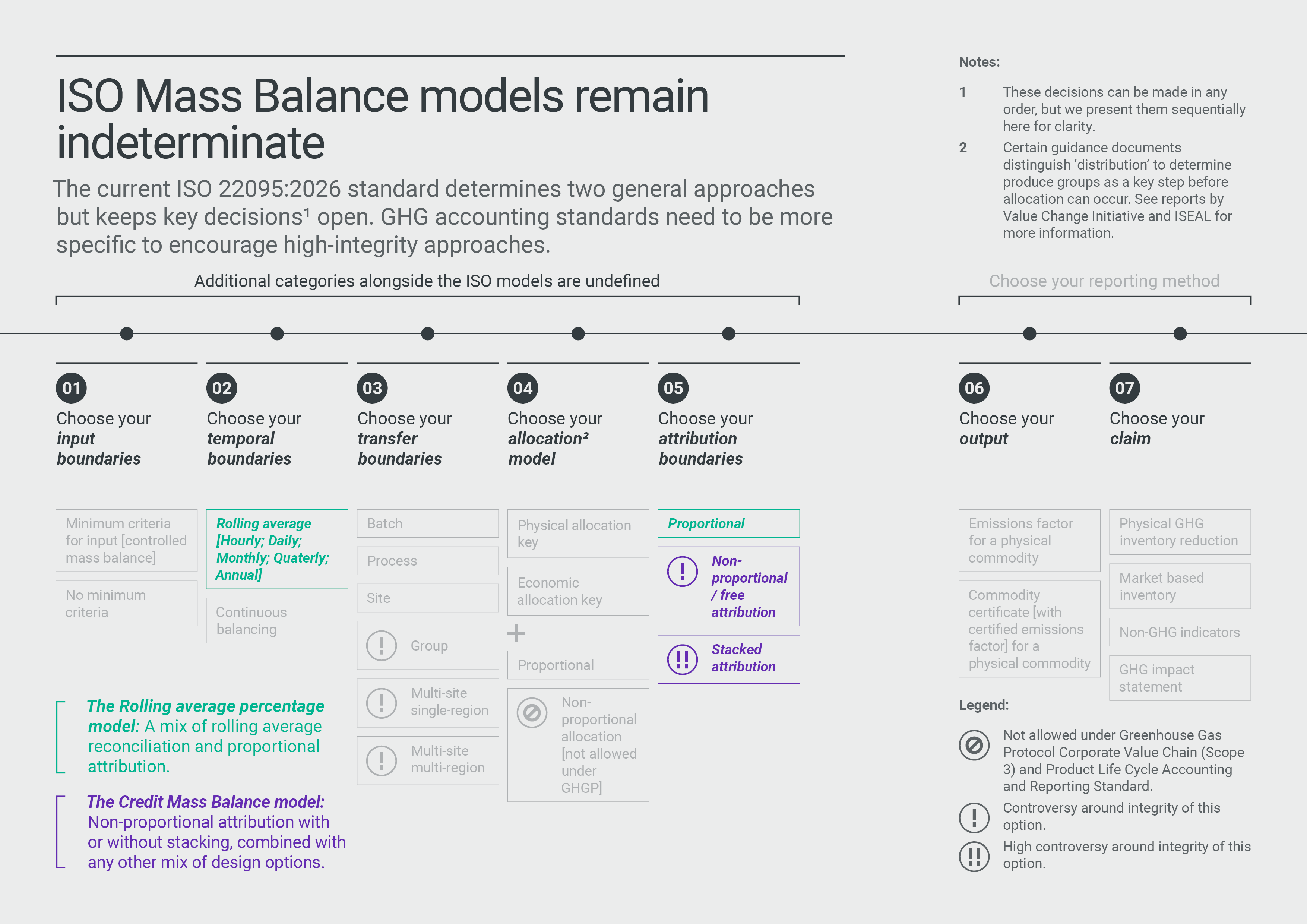

Existing standards on mass balance remain vague on key decisions

The International Organisation for Standardization (ISO) standard number 22095-2:2026 illustrates this challenge. While it offers a general definition of chain of custody terminology, it is not specific to emissions accounting. The standard outlines two types of mass balance: 1) the rolling average percentage method and 2) the credit mass balance model (see Figure 2). These approaches only specify certain criteria as illustrated in green and purple, while leaving other critical decisions open. For example, the ‘credit mass balance model’ could allow for the non-proportional attribution of emissions reductions based on a genuine technological intervention. However, it could also allow stacked attribution that is highly exaggerated and misleading.

To properly evaluate the integrity of these models, more nuanced guidance is needed on how these open decisions should be resolved in specific contexts. A growing number of sectoral guidance documents and standards on mass balance, such as the Land Sector Removal Guidance or the World Steel association guidelines are attempting to add nuance, but their requirements still vary in levels of specificity and detail.

Fig 2: ISO Mass balance models

Can mass balance drive system-wide decarbonisation?

Whether mass balance accounting enables or delays decarbonisation ultimately depends on the standards and how they are put into practice. The GHG Protocol’s ongoing development of guidance for the use of Actions and Market Instruments represents a critical window to get this right. Based on our analysis, there are several potential safeguards that can help strengthen integrity:

-

Set clear red lines: Stacked attribution (decision 6) should not be allowed to ensure that a final emissions profile is not lower than its lowest-emissions input entering the system.

-

Use mass balance as a transitional tool: Mass balance can support targeted transitions to breakthrough emissions reduction technologies or emissions accounting in sectors where structural challenges limit traceability. However, it should not become a permanent substitute for improved traceability or decarbonisation efforts across the entire value chain.

-

Develop sector-specific guidance: What constitutes a high-integrity mass balance model in steel may be physically unfeasible in agriculture and vice versa. For example, the use of wide transfer boundaries may be appropriate in the agriculture sector where integrating smallholder farmers into emissions accounting frameworks can be challenging. Standards should recognise different technological transition pathways without lowering the bar for ease of adoption in more complex sectors as this risks creating loopholes that undermine integrity across the board. Beyond high level integrity principles, the GHG Protocol's ability to set detailed sector-specific rules may be limited. It is therefore essential for sector-specific standards to offer more nuanced guidance.

-

Increase transparency and verification: Companies producing commodities using mass balance, as well as companies buying these commodities, should disclose the method’s underlying features. Companies like Volvo are already taking a more transparent approach to communication. Lack of transparency can carry significant reputational and legal risks. Consumers expecting products to be physically lower in emissions may feel misled if there is low likelihood that any low-carbon material is actually present in the final product.

-

Employ third party verification: Independent verification is a critical measure to ensure robustness. Business customers may increasingly need to substantiate low-carbon procurement claims, particularly with regards to potentially changing regulations.

At its best, mass balance could be a pragmatic bridge between current and future decarbonisation. At its worst, it could become the very mechanism that delays real change by enabling weak or misleading claims. Crucially, the ISO definitions of ‘rolling average’ and ‘credit mass balance’ do not reflect the nuances that are integral to this difference. The decarbonisation impact of mass balance systems depends on context and on the specific rules and safeguards set by the sectoral standards governing these systems.

The next blog post in this series will look at book-and-claim methods.